Immediate Action Item for States: Review Your Provider Tax Statutes and Regulations

Consider if the State wants to continue to fund Medicaid through provider taxes after the enactment of the Budget Reconciliation. If Provider Taxes are part of future state Medicaid funding plans, action may be required before the Bill is signed.

Understanding Provider Taxes and Federal Requirements

The primary reduction in federal Medicaid costs results from two separate sections of the Bill, both related to provider taxes. Currently, every state except Alaska levies some level of taxes on segments of its health care providers, and those taxes are generally used to pay for part of the state share of various Medicaid programs.1 The taxes are permissible state funding for Medicaid under federal law if they:

- Are imposed on a permissible class,

- Are broad based and uniform (unless a waiver is granted), and

- Do not hold taxpayers harmless.

These last two requirements we interpreted by CMS via rule-making process in 1993, and statistical tests were established to implement them. Since that time, States have designed programs and requested waivers that meet these tests, but which have the effect of taxing Medicaid providers significantly more—as they are the ones that will receive the revenue back from the state in the form of Medicaid payments. Essentially by receiving a waiver for taxes that aren’t broad based or uniform, states are effectively holding taxpaying providers harmless.

Impact of CMS Changes and Proposed Rule-making

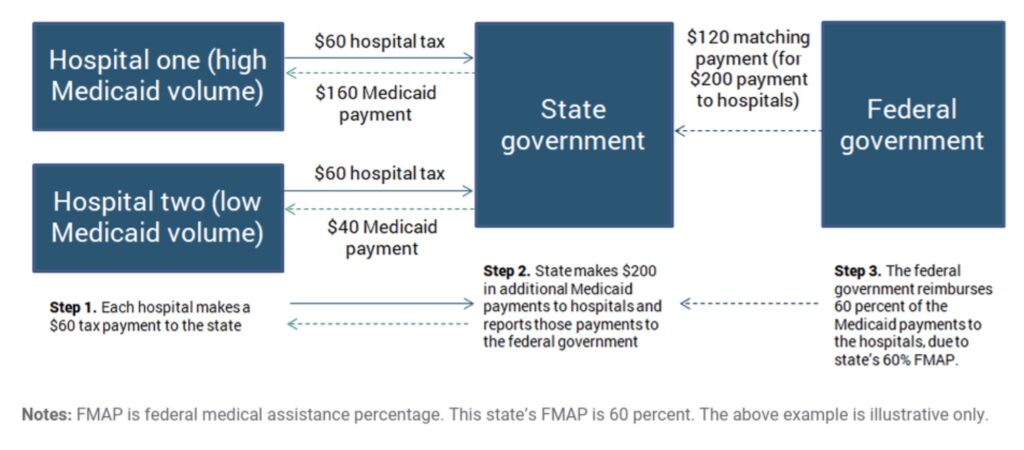

States implement these taxes because they have the effect of increasing the federal cost of Medicaid and lowering the state cost. The graphic below, from the Medicaid and CHIP Payment Access Commission, illustrates the process for a Provider Tax that meets all three of the federal requirements.

Figure 1: Illustration of a Permissible Health Care-Related Tax Arrangement for Hospitals with Different Medicaid Volumes2

If, instead of the process shown above, the state levies either higher taxes of Hospital one, or exempts Hospital two from some or all tax payments, the State and Hospital two are both better off, and Hospital 2 is indirectly “held harmless.”

Under what CMS considers the “spirit” of laws regarding provider taxes, many states set provider taxes to indirectly hold low-Medicaid volume providers harmless. The CMS tests for whether it will issue a waiver to the “broad based” and “uniform” provider taxes created statistical “loopholes” that states have used. This practice is widespread and used by states controlled by both parties. For example:

- California set a tax on Managed Care Organizations (MCO) for mid-sized providers with significant Medicaid enrollment at $274 per member month, while similar sized providers with few Medicaid enrollees are changed between $1.75 and $2.25 per member month. This proposal, based on information provided by the State, caused CMS to determine that “…99% of the tax burden” to fall on Medicaid member months, increasing federal financial participation received by California while effectively holding harmless providers.3

- Iowa statute specifically sets its “quality assurance fee” [provider tax] on nursing facilities to the federal regulatory cite for the upper limit before the “hold harmless” requirement will be violated (automatically changing it has the regulations change). It sets each nursing facility’s assessment amount after including consideration of the amount that the provider has received in Medicaid funding. In addition, the law states, “A nursing facility shall not knowingly pass on the quality assurance assessment to non-Medicaid payors, including as a rate increase or service charge.” This allows a nursing facility to pass on this fee only to Medicaid payors.4

CMS, under administrations of both parties, has identified these “loopholes” and has announced steps to change the regulations.5 Most recently, on May 15, 2025, CMS issued a Notice of Proposed Rulemaking (NPRM) proposing significant changes.6 Under the newly proposed rule, CMS would close this “loophole” and provide a transition period, allowing their Medicaid agencies and legislatures time to modify their provider taxes to bring them into compliance with the new final rules, when announced.7

Legislative Developments on the Provider Tax: Bill Sections and Their Implications

Bill Section 44134 “Requirements Regarding Waiver of Uniform Tax Requirement for Medicaid Provider’s Tax” it Congress’ statutory, rather than regulatory, method of closing the loophole. The section would explicitly prevent CMS from issuing any waivers to states that directly or indirectly setting provider taxes differently for low and high Medicaid volume providers. Section 44134 goes into effect on the enactment of the Bill, but allows the Secretary of HHS to implement a transition period, as appropriate, of up to three fiscal years.

Despite section 44134 allowing for a transition period, states looking to replace revenues from non-conforming provider taxes may not be able to practically replace them with conforming provider taxes. A different Bill section, Section 44132, requires that federal financial contributions to a state be reduced proportionate to any state revenues from a new or increased broad-based health care related tax passed after the date of the Bill’s enactment. It is unclear how this will be interpreted, but it appears that increasing the tax on non-Medicaid providers (which previously might have paid a lower rate) would not be permitted. As a result, if a state has non-conforming provider taxes as the time of the Bill’s passage, this section may prevent them from replacing existing taxes with conforming provider taxes that use the permissible Medicaid funding mechanism showed in Figure 1 above. If a state already has a conforming provider tax at the time of the Bill’s enactment, the funding process in Figure 1 will apply. This gives a strong incentive for states to quickly examine and potentially change their provider taxes.

State Medicaid agencies, governors, and legislatures should be aware of this significant timing constraint. If the State is interested in funding a portion of its Medicaid costs with provider tax revenue that is not counted against federal financial participation, the state should closely examine the structure of its current provider taxes, and determine if immediate changes are needed.

Changes Not Related to the Provider Tax

Our analysis shows that many of the discussed federal cost reductions result from fewer program enrollees—cost reductions that would also apply to states, although states would also face the increased administrative costs associated with churn. The state-by-state impact of changes to redetermination processes, the addition of work requirements for the expansion population, and restrictions on MCO premiums will vary greatly. Medicaid agencies are facing down a large amount of detailed scenario analysis that will need to pull together a wide array of both the Medicaid agency’s data, demographic data, and other supplemental datasets.

The Role of Data Analysis in Medicaid Impact Assessment

Resultant’s data analysis experts have been partnering with our legislative policy wonks to identify the best data and iterative approach to estimating the costs an individual state will face from changes the Bill introduces. The types of “what if” analysis that will bring together both increased and decreased services costs, increased administrative costs, and different state funding options that will impact the cost of provider services is well beyond what can effectively and efficiently be done in most Medicaid program’s favorite tool—Excel. The Resultant data analytics experts welcome the opportunity to work with you on how to best run scenario analyses to predict, plan for, and help your legislature and governor make the best decisions in light of these changes.

The table below summarizes the sections of the Committee Print of the House Energy and Commerce Medicaid proposal.

VIEW THE TABLE HERE

About Resultant

We know that data begins as chaos—but in expert hands, it transforms into insight that solves problems, drives progress, and makes life and work exponentially better. Resultant is a modern consulting firm with a radically different approach to solving problems. Our team believes solutions are more valuable, transformative, and meaningful when reached together. Through outcomes built on solutions rooted in data analytics, technology, and management consulting, Resultant serves as a true partner by solving problems with our clients, rather than for them.

Together, we partner with clients in the public and private sectors to help them overcome their most complex challenges, empowering our clients to drive meaningful change in their organizations and communities.

1 DC also levies provider taxes.

2 MACPAC, “IssueBrief: Health Care-Related Taxes in Medicaid,” May, 2021, https://www.macpac.gov/wp-content/uploads/2020/01/Health-Care-Related-Taxes-in-Medicaid.pdf

3 Letter from CMS to Tyler Sadwith, December 20, 2024, https://www.dhcs.ca.gov/services/Documents/1903w3B-and-C-MCO-Tax-2023-2026-Amendment.pdf

4 IA Code § 249L.3 and IA Code § 249L.4 (2024)

5 Tsai, Daniel, “CMCS Informational Bulletin: Health Care-Related Taxes and Hold Harmless Arrangements Involving the Redistribution of Medicaid Payments,” February 17 2023. https://www.medicaid.gov/sites/default/files/2023-02/cib021723.pdf and “Preserving Medicaid Funding for Vulnerable Populations—Closing a Health Care-Related Tax Loophole Proposed Rule,” Federal Register 90 No. 93 (Thursday, May 15, 2025) 20578 https://www.federalregister.gov/documents/2025/05/15/2025-08566/medicaid-program-preserving-medicaid-funding-for-vulnerable-populations-closing-a-health

6 Ibid.

7 Ibid. CMS has excluded 4 unnamed states from its transition period. Resultant has identified California as one of the four states that will not receive a transition period under the NPRM as proposed. States not eligible for a transition period are identified those receiving CMS waivers on their provider taxes within the last 2 years and receiving with their waiver a companion letter warning them of the impending rule changes that may invalidate their tax in the future.

About the author